Lawn Mower Loans: Financing Your Next Mower

Explore lawn mower loans, compare store financing, personal loans, and cards, and pick the option that minimizes cost. Practical tips, examples, and a clear buying guide from Mower Help.

Lawn mower loans are financing options that let you spread the cost of a mower over time rather than paying upfront. The three most common routes are store financing at retailers, unsecured personal loans, and credit cards with promotional APRs. To minimize total cost, compare APRs, fees, repayment terms, and promo offers. Favor transparent lenders who allow early payoff without penalties, and beware promo traps that reset rates after the teaser period.

The Financial Why: When Financing Makes Sense

Financing a lawn mower can help you buy a higher-quality model earlier than you could with cash. It also helps you spread maintenance costs across more manageable monthly payments. However, loans are a two-edged sword: you pay interest and possibly fees, which add to the total price. The decision to pursue lawn mower loans should be guided by your budget, the mower’s expected lifespan, and how quickly you can recoup time savings from a faster, more reliable machine. If you anticipate lawn work during peak seasons and foresee major maintenance, spreading those costs can smooth irregular cash flows. The team also notes that promotional financing—such as short-term zero-APR periods—can make sense when you can pay off before the promotional period ends. Otherwise, standard loans with modest interest can be preferable to high-interest cards. According to Mower Help, loans should be used deliberately to improve purchasing power without overspending.

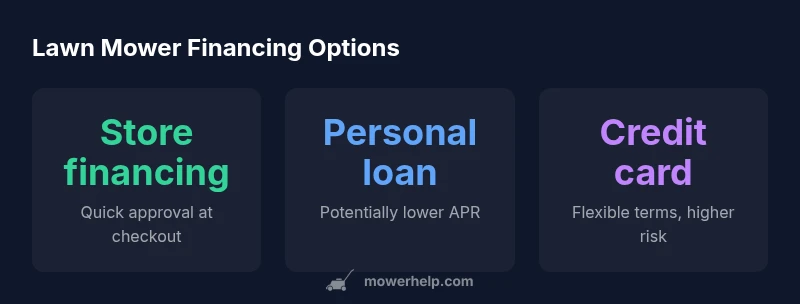

Financing options at a glance

There are several paths to fund a mower purchase, and each has distinct logistics. The three most common routes are:

- Store financing at the retailer, which can offer quick approvals and bundled warranties, but may come with higher long-term costs if you miss promo terms or pay beyond the promo window.

- Unsecured personal loans from banks or online lenders, typically with transparent terms and possibly lower rates for strong credit, though they require credit checks.

- Credit cards with promotional APRs, which can be convenient for small purchases but may carry higher ongoing rates if the balance isn’t paid off in time.

Key tips: compare total costs, read the fine print for fees, and factor in any extended-warranty costs or required maintenance packages. The right choice depends on your timeline, budget, and risk tolerance.

Store financing vs personal loans: Pros and Cons

Store financing offers speed and convenience—often a same-day decision at the point of sale. However, it can lock you into merchant-specific terms or higher interest once promotional periods end. Personal loans, especially from traditional banks or reputable online lenders, can provide competitive APRs and flexible use; they also carry a broader set of repayment terms. The downside is a credit check and potential origination fees.

Credit cards with promotional APRs can provide large upfront flexibility but demand discipline: high APRs apply after the promo period ends, and carrying a balance can quickly become expensive. A mixed approach—using store financing for promotions and a separate loan for the remainder—can be a savvy strategy if you never let the promo terms lapse.

Credit considerations and how to prepare

Before applying for any lawn mower loan, review your credit health. Lenders typically assess your credit score, income stability, and existing debt. A clean personal financial picture with steady income and minimal revolving debt improves approval odds and can unlock better terms. Gather supporting documents: recent pay stubs, tax returns, bank statements, and a list of current debts. If your score isn’t ideal, you can still qualify for certain programs or smaller loan amounts, but expect higher rates or stricter terms. Proactively addressing any errors on your credit report and paying down high-interest balances can pay off before applying.

How to estimate payments without guessing

A practical way to forecast payments is to use the standard loan payment formula: Monthly payment = P × r / (1 − (1 + r)^−n), where P is the loan amount, r is the monthly interest rate (annual rate divided by 12), and n is the number of payments. Replace placeholders with your terms to see how price, rate, and term affect monthly cost. If you’re testing options, plug in different APRs and terms to compare total costs over the life of each loan. Always account for taxes, delivery, and potential maintenance add-ons that can alter the total price.

Comparing offers: what to look for

When evaluating mower financing, prioritize these criteria:

- APR and total interest paid over the life of the loan

- Any origination, processing, or prepayment penalties

- Term length and the number of payments

- Fees associated with late payments or balance transfers

- Promo period conditions and whether you can pay off early without penalty

- Added protections like extended warranties or service packages included in the deal

A simple rule: the lowest total cost wins, not the lowest monthly payment.

Alternatives to loans you can consider

If debt isn’t desirable, consider cost-saving approaches first:

- Save gradually for a cash purchase or larger down payment to reduce loan size

- Explore discounted used mowers from reputable dealers, ensuring a proper inspection and history

- Rent-to-own or short-term rental programs for seasonal needs

- Look for seasonal promotions, bundle offers with maintenance kits, or financing that aligns with tax refunds

Each alternative has trade-offs in terms of depreciation, warranty coverage, and maintenance costs. Compare total ownership costs over the mower’s expected lifespan.

The application process: step-by-step

Applying for lawn mower financing can be straightforward:

- Define your budget and the mower model you want

- Gather income verification and ID documents

- Compare three to five offers from different lenders or retailers

- Apply and review pre-approval terms without affecting your credit score much (soft pulls)

- Choose the best offer and complete the funding paperwork

- Accept delivery and set up automatic payments to avoid late fees

Preparation reduces friction and helps you secure favorable terms.

Common mistakes to avoid and practical tips

Avoid common financing pitfalls: jumping on the lowest monthly payment without evaluating total costs, ignoring promotional end dates, or assuming all offers are the same. Read the fine print about penalties, service packages, and warranty coverage. Don’t signs a loan with a high penalty for early payoff just to secure a deal. The Mower Help team emphasizes building a clear payoff plan and staying within a realistic monthly budget to prevent debt from escalating.

Comparison of lawn mower financing options

| Option | What it is | Pros | Cons |

|---|---|---|---|

| Store Financing | Financing offered directly by retailers at checkout | Convenient; quick approval; sometimes bundled incentives | May have higher long-term costs; terms vary by store |

| Personal Loan | Unsecured loan from bank or online lender | Transparent terms; potential lower APR; flexible use | Requires credit check; possible origination fees |

| Credit Card Financing | Credit card with promotional terms for a purchase | Fast decisions; can be a simple checkout option | Higher APR after promo ends; risk of debt |

| Lease/Other | Equipment lease or rental program | Low upfront cost; predictable monthly payments | Long-term costs; depreciation; limits on ownership |

Got Questions?

What factors should I consider before taking a lawn mower loan?

Before applying, compare the total cost across options, check for hidden fees, and ensure the monthly payments fit your budget. Assess how long you will own the mower and whether a promo period makes sense for your timeline.

Compare total cost and ensure monthly payments fit your budget.

Are 0% financing offers worth it?

0% offers are beneficial only if you can pay off the balance before the promo ends and there are no hidden fees. If you cannot pay off early, the standard rate after the promo may be higher than alternative options.

Only if you can pay within the promo period and avoid extra fees.

Do I need a high credit score to qualify for lawn mower loans?

Qualification varies by lender. Some programs accept fair credit with higher rates, while others require good credit for the best terms. Always check multiple lenders to see which fits your profile.

Qualifications vary; shop around for the best match.

Can I use a personal loan to buy a mower?

Yes. A personal loan can offer flexible use and potentially lower rates for strong credit. Compare terms with store financing to determine overall cost and risk.

Yes, compare it to store financing to see which is cheaper overall.

What if I want to upgrade to a better mower later?

If you anticipate upgrading, consider loan terms that allow early payoff or refinancing without penalties. A flexible plan helps you avoid being stuck with an unwanted model.

Choose terms that allow payoff or refinancing without penalties.

Are there cheaper alternatives to financing?

Saving toward the purchase, buying a certified used mower with solid warranty, or waiting for non-financed promotions can reduce total costs. Weigh depreciation and maintenance when considering alternatives.

Consider saving, warranties, and promotions before financing.

“Financing a lawn mower can be sensible when you compare total costs across options and avoid high-interest debt.”

The Essentials

- Define budget and desired mower features before shopping

- Compare total cost, not just monthly payments

- Watch promo periods and avoid penalties

- Consider alternatives to loans when possible

- Use a trusted guide (like Mower Help) to evaluate offers